Our TLDR

A lot more investment is needed to decarbonize the heat used to power the industrial sectors we rely on for food, infrastructure, materials, clothing, medicine, and more. We spoke with dozens of industry incumbents, innovators, and policymakers to form a unique view on what an industrial heat startup needs to have to fit the venture model. We cover why startups tackling industrial heat decarbonization are underfunded relative to emissions abatement potential, and our view on whether these emerging companies are good venture capital investments.

Here’s what we screen for at Congruent:

- Process Integration: Solutions that are modular and can replace existing systems with minimal friction are the most likely to overcome customer adoption hurdles.

- Business Continuity: Technologies that maintain reliable heat and do not threaten to disrupt plant operations are table stakes.

- Financial Viability: Zero upfront CapEx is best, but if CapEx is required, we believe customers will look for payback periods between 3-5 years (or less) to consider an investment.

- Technology Risk: We look for technologies in the sector that are already de-risked or will not require a substantial amount ($20+ million) of additional equity to reach commercial pilot.

If a company checks all four of these boxes, it may be a fit for our portfolio.

The hotter the better?

Not necessarily. While higher heat is typically linked to higher abatement potential, we believe there are compelling companies across the entire heat spectrum (from food to steel). Each industrial sector has unique challenges to deploy clean heat technologies, but the common denominator among them is a large TAM that may have significant revenue potential.

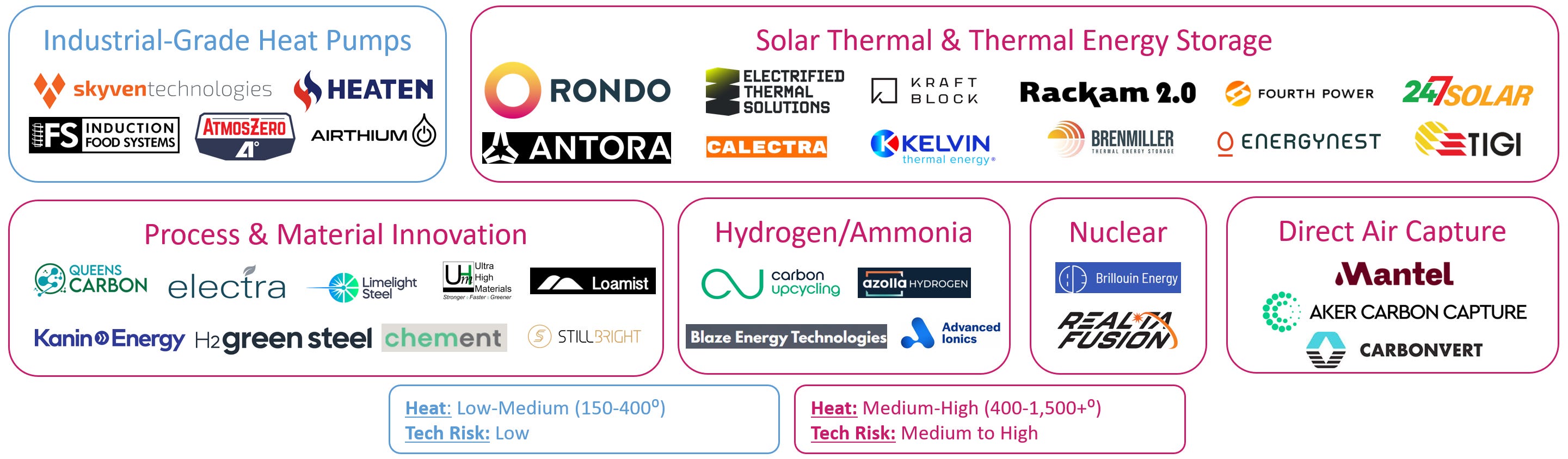

Selected Industrial Heat Innovation Areas

For companies targeting low-medium heat sectors (typically food, paper, chemicals, textiles, pharma), we prioritize proven technologies and innovative go to market strategies that address key adoption obstacles (e.g., industrial grade heat pumps). Specifically, we’ve seen structured financing and equipment leasing structures that reduce or eliminate upfront costs while enabling energy savings and carbon reduction. Since these technologies already exist and are commercially deployable today, they may have lower customer adoption hurdles and faster growth trajectories. Companies operating here need to be able to prove a defensible, sustainable margin profile as penetration and competition scale.

For companies targeting high heat sectors (typically steel, cement, glass), there is inevitably more technology risk that exacerbates the challenge of commercializing on a venture timeline (e.g., thermal energy storage, hydrogen). However, Congruent doesn’t shy away from investments with technology risk, particularly when we have high conviction in a team’s ability to hit early technical milestones such as industrial pilot projects. When looking at high tech risk opportunities, we like to see incremental investment dollars materially reduce risk at every step along the development path. Companies that need to build a full-scale plant before economics are clear may not be a fit for us. The notable tailwinds behind industrial decarbonization from policy to cost volatility reduction are further catalysts that can make investment in first-of-a-kind technology uniquely timely today (more on this below).

Industrial Heat Background

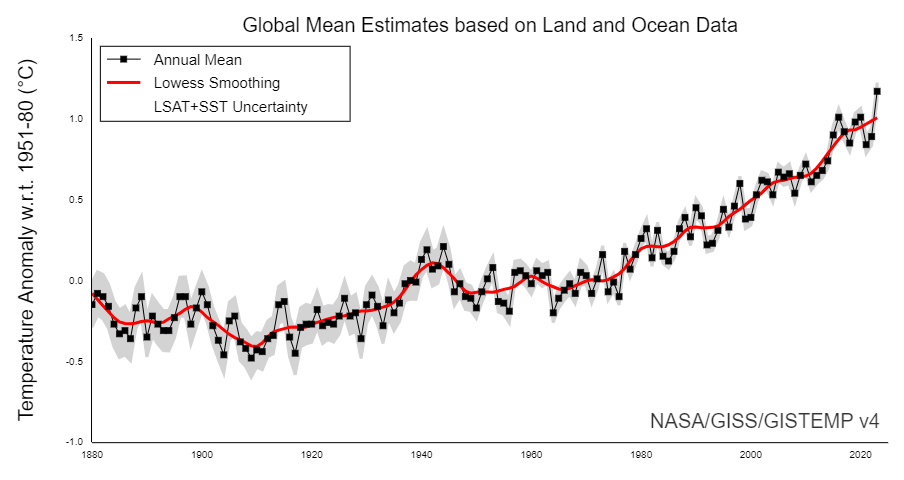

There’s a reason why the Paris Agreement benchmarks its global temperature increase limit of 1.5°C to “pre-industrial” levels. The Second Industrial Revolution (~1870-1914) followed by World War I (1914-1918), was an extended period of mass-production for cement, steel, and consumer goods. This marked the start of the industrial sector’s significant and consistent contribution to fossil fuel emissions and climate change over the past century.

Global Temperature Mean Since the Second Industrial Revolution1

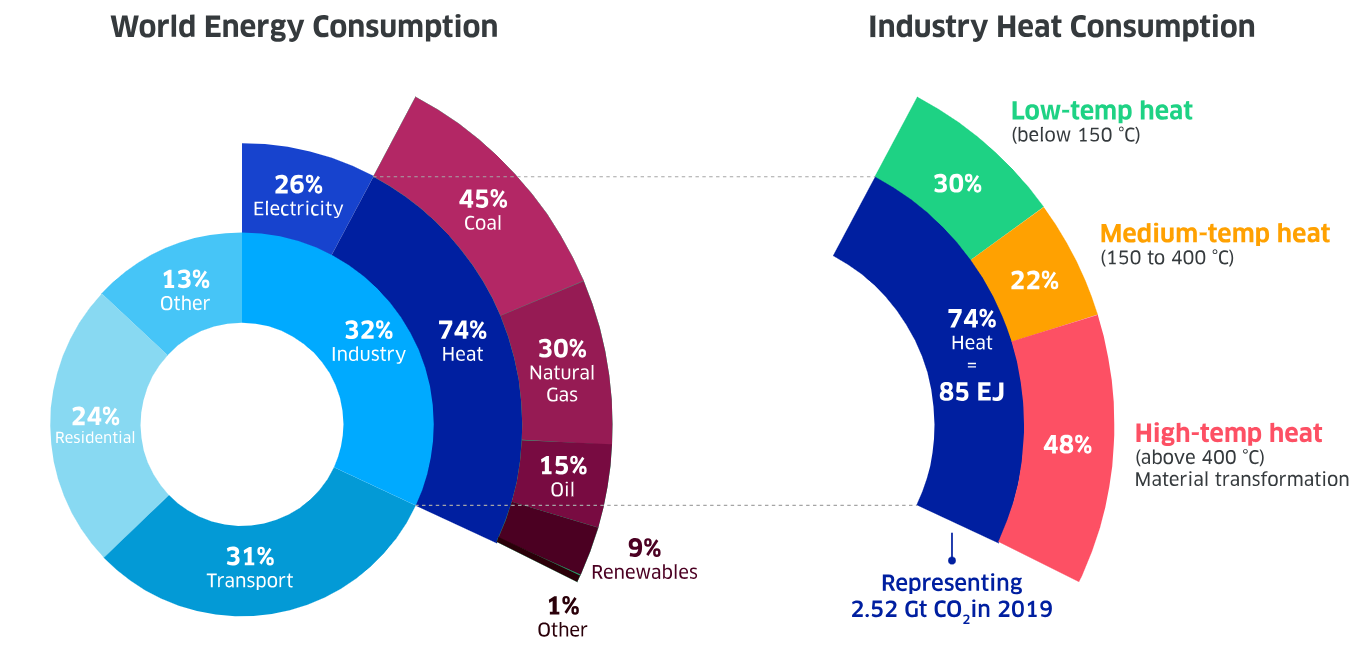

Globally, industrial processes consume roughly one-third of all energy and heat represents ~75% of the sector’s energy consumption. Today, 90% of this energy is still generated by fossil fuels. Industrial processes require heat at a wide range of temperatures, roughly 50% “low-heat” and 50% “high-heat.” Sectors like food, paper, chemicals, textiles, and pharmaceuticals require low-temperature heat below 200°C to power processes such as washing, drying, and sterilization. Sectors such as steel, cement, and glass require high-temperature heat well above 1,000°C to enable material transformation such as melting iron ore to form steel.

Industry Leads Global Energy Consumption 2

As venture capital investors, we recognize a large opportunity to decarbonize industrial process heat by replacing fossil-based incumbent technologies with low carbon alternatives over the next decade. However, industrial heat is one of the most difficult areas to decarbonize, particularly when high temperatures are required, for a variety of reasons. In our view, the most notable impediments to clean technology deployment are 1) customer adoption, 2) cost, and 3) time to deploy. This is perhaps why there is a significant shortfall between the investment dollars earned by industrial heat startups relative to their emissions abatement potential.

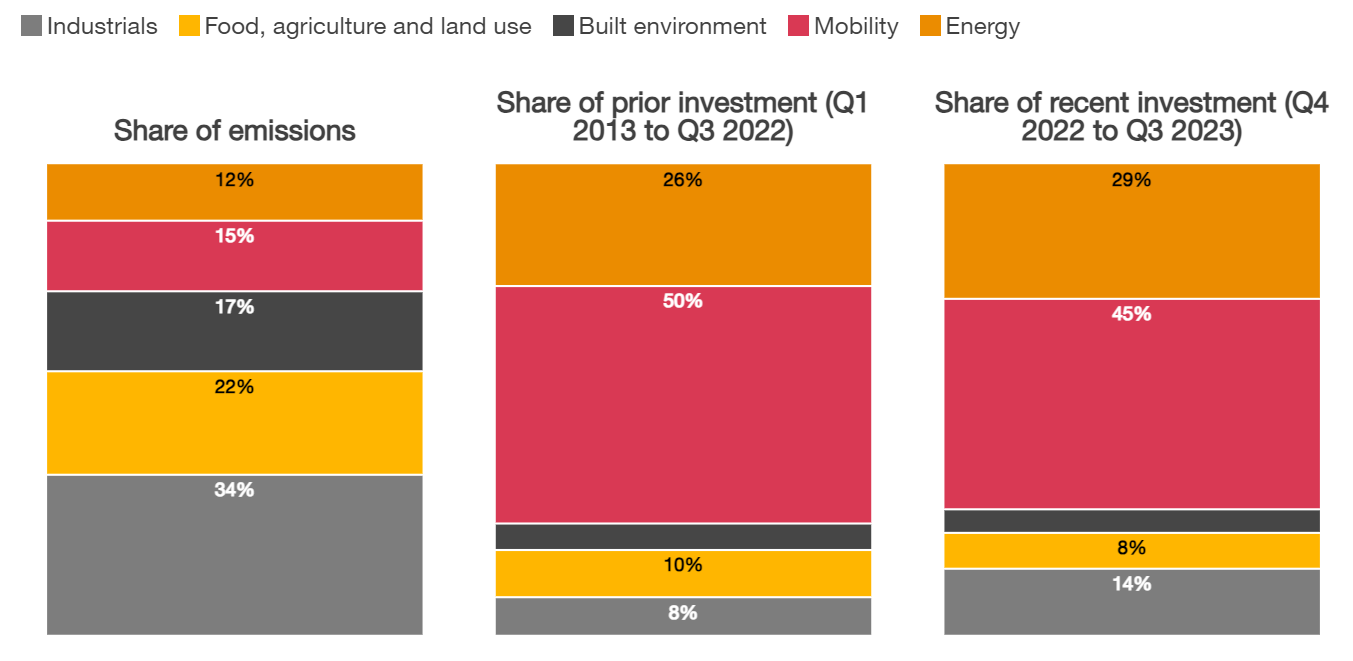

Abatement Potential Funding Gap 3

Heavy industry received only 8% of overall venture capital investment between Q1 2013 and Q3 2022 despite contributing over one-third of global emissions. While this number ticked up to 14% between Q4 2022 and Q3 2023, it is still substantially below where it should be relative to total emissions. For comparison, mobility has received roughly half of all investment despite only generating 15% of global emissions.

Congruent’s Bull & Bear Perspectives

There are many reasons the decarbonization of industrial process heat could be an exciting area for early-stage venture investment. At the same time, there are certain dynamics underlying industrial heat that could inhibit venture-scale outcomes for emerging companies. We’ve summarized our Bear and Bull views on this market below:

Enablers (Bull View)

- Large TAM: We estimate that $500 billion or more of total CapEx will be needed to decarbonize industrial process heat. Our internal analysis suggests total CapEx of $300 billion just to replace existing boiler capacity with industrial grade heat pumps 4,5. We estimate the opportunity for other low-medium heat technologies and emerging high heat solutions to be similar based on per plant CapEx of $1-50 million and the US plant footprint across industrial sectors.

- Government Funding: While we don’t overly credit access to government funding in our investment decisions, it can be a critical tailwind at the earliest stages where we invest. $6 billion is earmarked under the IRA for early-stage commercial-scale industrial demonstration projects and $10 billion is available from investment tax credits for eligible projects under 48C, both encompassing industrial heat.

- Regulatory Tailwinds: There are several notable examples of favorable cross-state and cross-border regulations underpinning industrial demand for clean heat. CA SB 253 will require over 5,000 businesses operating in California to report Scope 1-3 emissions beginning next year. CBAM in Europe will incentivize industrial importers to decarbonize faster to avoid tariffs beginning in 2026. For industrial companies with foresight, this type of policy should stimulate attention and investment of resources toward decarbonizing heat.

- Technology Availability: Several technologies that can be used to decarbonize low- and medium-heat sectors, such as industrial heat pumps, are largely de-risked and ready to commercially deploy today. These technologies can also be more efficient than their natural gas counterparts. For example, industrial heat pumps have a coefficient of performance of 3x compared to <1x for natural gas, meaning that heat pumps can more efficiently turn power into heat 6. This often overcomes the spark spread where methane is less expensive per BTU than electricity, but less efficient in converting that energy to usable heat.

- Offtake Commitments: Coalitions such as the First Movers Coalition can create early market demand to bring emerging industrial heat decarbonization technology to commercial scale.

Obstacles (Bear View)

- Customer Adoption: Industrial customers will simply not disrupt existing processes, jeopardize business continuity, take unnecessary technology risk, and spend additional CapEx/OpEx to decarbonize their heat. Industrial processes require constant heat, operate with razor thin margins, and thus have a high cost of failure. There is also an acute sense of inertia, lack of awareness, and resistance to change more generally that will take time to shift.

- High CapEx: As mentioned previously, we estimate CapEx per plant to be $1-50 million. Manufacturing facilities often have very low operating margins and low CapEx budgets creating a funding mismatch. Decision makers are either unwilling or unable to commit large dollars to these types of projects.

- Unit Economics: Natural gas is still the cheapest way to generate industrial heat in many manufacturing-heavy regions in the US, creating a further disincentive for decision-makers to pursue alternative forms of energy for heat generation. The lower the natural gas price, the lower the value of cost savings and longer the payback relative to the capital cost of a clean alternative.

- Technology Risk: The high-heat segment specifically requires advanced innovation beyond mainstream engineering that is talent-constrained and may take longer than 10 years to successfully commercialize.

- Infrastructure Risk: Electrifying processes currently powered by fossil fuel will take a significant amount of electricity, perhaps in excess of what the current grid can support. Building out a higher capacity grid will take time and likely significant regulatory and permitting support and reform.

Final Thoughts

We’re excited to see so many startups tackling the problem of industrial heat from all angles. As venture investors, we look for companies that can scale quickly to billion-dollar outcomes. While we have not found a company that fits our investment criteria for this category, we do believe status quo changing companies will emerge. We are fueled to continue tracking investment opportunities in the space based on large addressable market opportunities and urgency for decarbonization. If you are an innovator working on a solution to industrial heat, we’d love to hear from you!

Sources

- NASA

- Engie Impact

- IPCC, Pitchbook, PwC Analysis

- Department of Energy

- NREL. Assumes heat pump cost of $50-$200k per MMBtu of heat delivered.

- Renewable Thermal Collective: Industrial Thermal Decarbonization Package